The BendDAO bank run 💥

BendDAO's credit crunch explained!

Metaversal is a Bankless newsletter for weekly level-ups on NFTs, virtual worlds, & collectibles

Dear Bankless Nation,

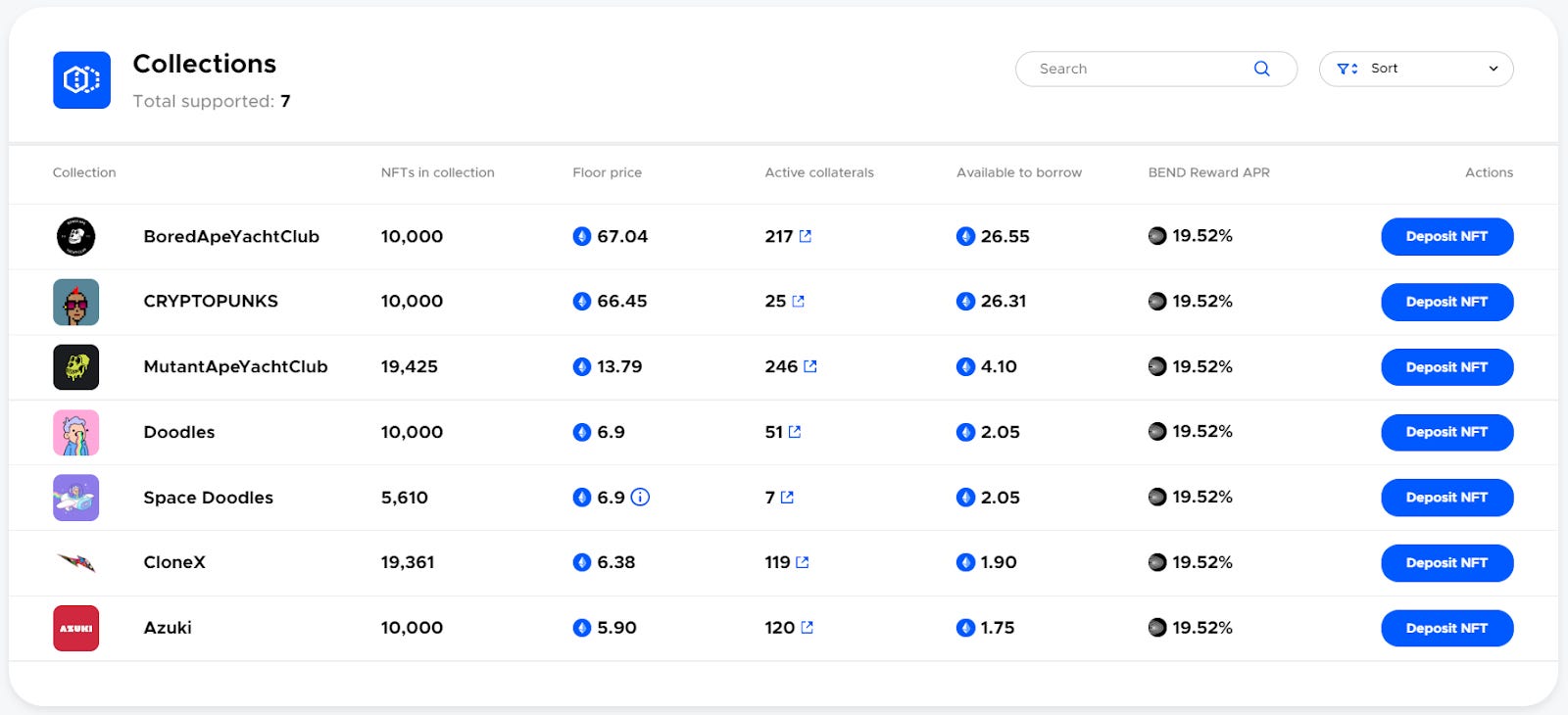

BendDAO is an NFT lending protocol.

Over the weekend, fears over bad debt thrust BendDAO into an on-chain bank run that saw its reserves drop from ~18,000 WETH to less than 15 WETH at one point.

This credit crunch threw BendDAO into crisis, leaving the project’s lenders and borrowers temporarily in the lurch. The good news is the protocol’s reserves are back up past 4.5k WETH at the time of this post’s writing, so the worst of the mess may be behind us.

However, this episode led to no shortage of doomful takes about the risks that BendDAO poses to the wider NFT ecosystem. Let’s cover what’s actually gone on and what to keep an eye on going forward for today’s Metaversal.

-WMP

🙏 Sponsor: Sequence—developer platform + smart wallet to build user-friendly web3 apps✨

An intro to the BendDAO crisis

What is BendDAO

BendDAO is an NFT liquidity protocol, i.e. an NFT borrowing and lending project.

Borrowers can use the dapp to borrow ETH against NFTs from seven top PFP NFT collections, namely Azuki, BAYC, CloneX, CryptoPunks, Doodles, MAYC, and Space Doodles.

Conversely, lenders can deposit ETH into the protocol’s liquidity pool to try and earn yield from the interest payments made by borrowers.

BendDAO accordingly makes use of a peer-to-pool model, which stands in contrast to the peer-to-peer lending style (i.e. where two individuals agree on negotiated terms) that initially came to the fore in the NFT ecosystem via projects like NFTfi.

This peer-to-pool approach underpins BendDAO’s three main offerings, which are instant NFT-backed loans (i.e. you don’t have to wait on peer-to-peer negotiations), collateral listings (i.e. get up to 40% of the floor value of your NFT before it actually sells), and NFT down payments (i.e. buy an NFT with a 60% down payment using a flashloan maneuver).

BendDAO’s bank run

BendDAO “underestimated how illiquid NFTs could be in a bear market when setting the initial parameters,” the team has since admitted.

The strictness of these first parameters led to a recent influx of bed debt (i.e. receiving NFTs instead of ETH because of failed liquidation auctions) into the DAO, which in turn led to the bank run we saw this past weekend — lenders saw the bad debt rising, and many promptly exited to get their deposited ETH out while there were still reserves left.

Why were the NFT auctions failing, then? Because of the initial BendDAO parameters that mandated default liquidation bids be higher than the debt outstanding against an NFT and be at least 95% of that NFT’s current floor value. As many collections’ floors have sagged downward recently, the debts against many BendDAO NFTs came to exceed these NFTs’ floor prices. Additionally, bids also had to be locked up for 48 hours.

These demands made these default auctions increasingly unattractive to liquidators, so BendDAO racked up more and more “bad debt” NFTs, and this in turn spooked many lenders to pull their deposits.

Making emergency adjustments

On August 23rd, BendDAO passed emergency parameter updates to progressively lower the liquidation threshold from 95% to a new final baseline of 70% as of September 20th. The DAO also agreed to lower the bidding lock-up period from 48 hours to four hours.

Ultimately, the end result of these adjustments will be to make BendDAO’s liquidation auctions more attractive for bidders and thus to keep ETH healthily flowing back into the protocol to avoid bad debt.

The big takeaway here, then? Over the coming weeks, it’s possible (depending on floor price performances) that we’ll see a surge in BendDAO liquidation auctions as it progressively becomes easier for BendDAO positions to default. If you’re in the market to buy top PFP NFTs, then pay attention to these auctions in the weeks ahead because there may be some heavily-discounted deals coming.

Back to normal now?

BendDAO is starting to rebound again after its emergency adjustments, plus recovering floor prices, have restored some confidence and deposit flows back into the platform.

Can the project thus return to a point where it can pay back all the lenders it still owes? At this point, that seems likely, though BendDAO isn’t necessarily out of the woods yet either. On the flip side, recent chatter around BendDAO contagion concerns have been vastly overblown.

Zooming out

The BendDAO credit crunch shows how the NFT lending sector is still very nascent, and while the field has many interesting innovations taking place within it, the projects therein are ultimately experiments until they become more battle-tested.

Unfortunately for BendDAO and its users, the protocol is getting quite the test in production right now on the heels of initially poor parameters, though the project may have already done enough to ultimately make it out of this storm in one piece. In the very least, you can guarantee this episode will go down as a big cautionary tale for other NFT peer-to-pool projects going forward.

Action steps

➰ Read the BendDAO docs to learn more about the project

🤳 Consider following NFTStatistics.eth and Cirrus on Twitter to track their BendDAO coverage going forward

🙇 See my latest Bankless tactic How to get liquidity on your NFTs

Author Bio

William M. Peaster is a professional writer and creator of Metaversal—a Bankless newsletter focused on the emergence of NFTs in the cryptoeconomy. He’s also recently been contributing content to Bankless, JPG, and beyond!

Subscribe to Bankless. $22 per mo. Includes archive access, Inner Circle & Badge.

🙏Thanks to our sponsor

Sequence

Build user-friendly web3 applications with ease and deliver a seamless web3 experience to your users! Sequence is a comprehensive developer platform and smart wallet for the Ethereum + EVM ecosystem.

Seamless and secure onboarding

No gas fees for your users

Direct NFT purchase with credit/debit

NFT marketplace protocol, and more tools, so you can deliver a seamless web3 experience to your users.

👉 Integrate Sequence Wallet into your app

👉 Make your web3 app user friendly with developer tools

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. Additionally, the Bankless writers hold crypto assets. See our investment disclosures here.

One thing to comment on is that it's pretty insane that they're considering changing the terms of these loans after the fact. For loans moving forward, fine, but I think there's a real legal issue at hand if they change the terms on people who have already agreed to different terms. It would set a dangerous precedent in DeFi.

why were lenders were allowed to withdraw their deposits? Not familiar with this DAO but if I provide 100 eth as a loan to an nft owner who in turn uses his nft as collateral to borrow 50 eth from me, how is it possible for me to “withdraw my deposit”?like brah this is free market capitalism you’re locked in!